Climate Risk Index for the Australian energy sector

20.02.2024 - 03:14

Mandala Partners (Mandala) in conjunction with Zurich Financial Services Australia (Zurich) has produced Australia’s first Climate Risk Index for the national energy generation sector. This report highlights the growing risk of climate change to the grid, how that risk is spread across the grid, and high-level options for mitigating those risks. More than 25% of Australia’s power generation assets are in the three highest categories for climate change risk.

"Australia’s energy generation assets underpin almost every aspect of economic and social interaction in the 21st century, however, much of the focus to date has centered on the risk of the energy grid to climate change, rather than on the risk of climate change to the grid."

- Justin Delaney, Chief Executive Officer, Zurich Australia & New Zealand

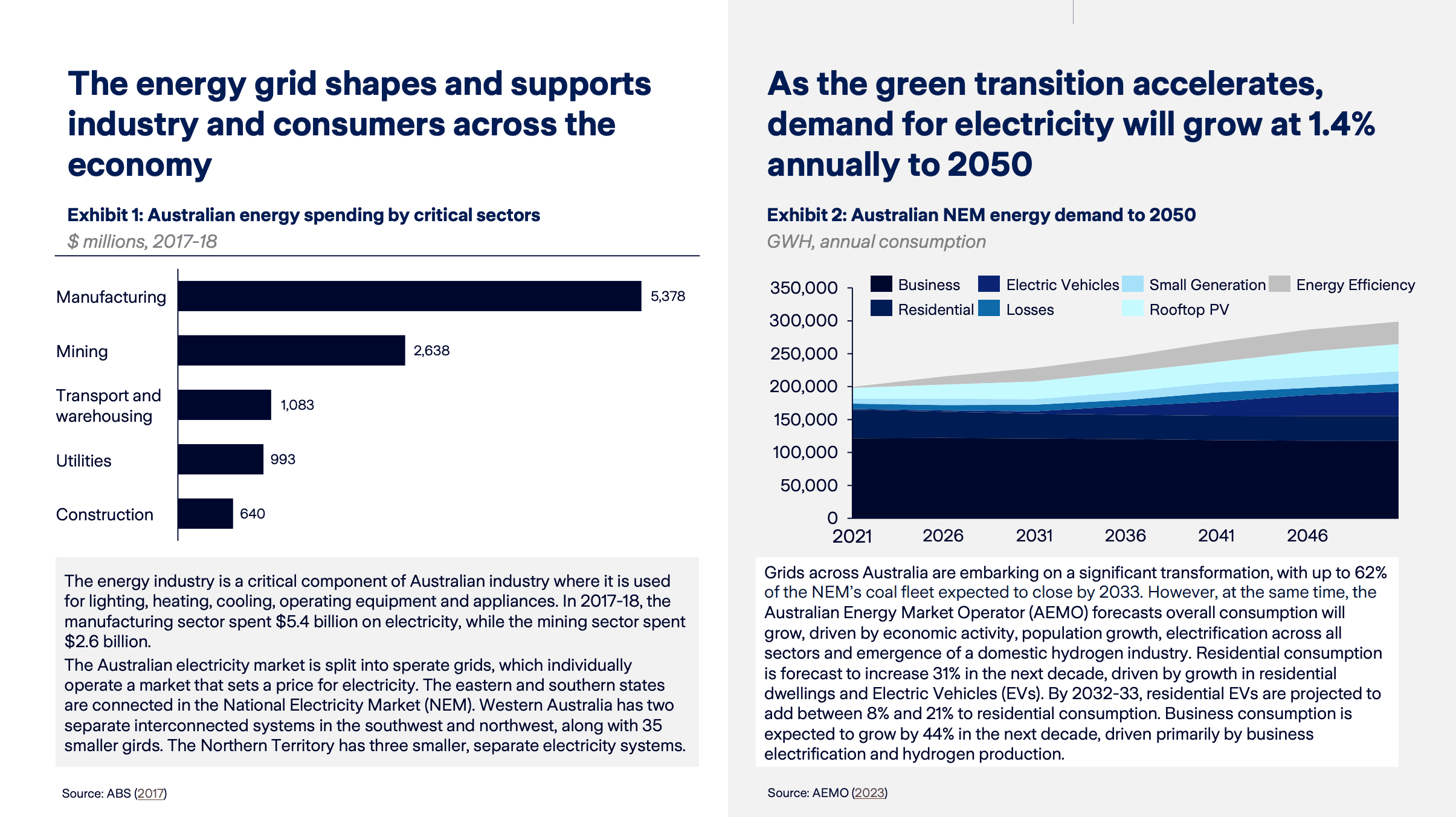

The Australian energy grid is critical to industry, consumers and the green transition

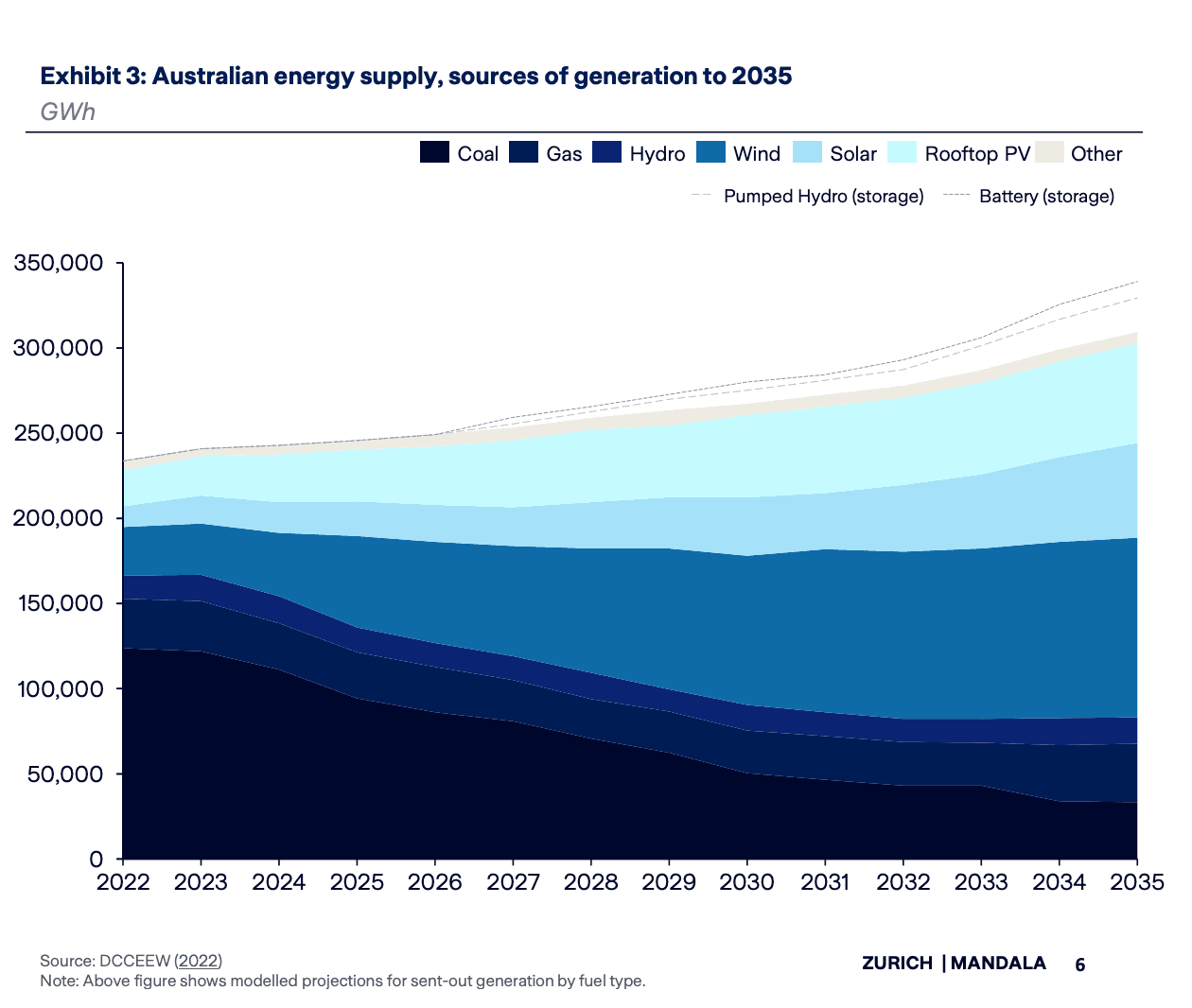

The last decade of energy policy has focused on transitioning to renewable energy sources and reducing prices for consumers. While prices have steadily climbed during this period, policies to transition the Australian grid have been fruitful.

During this period, the capacity of electricity generation from renewable sources has increased 215% from 26,700 GWh of generation in 2011-12 to 84,000 GWh in 2021-22. Under the Renewable Energy Target, this transition is required to accelerate with the goal to boost renewables to 82% of the grid by 2030.

This transition has been supported by the Australian Government’s green bank, the Clean Energy Finance Corporation (CEFC), which has invested more than $12.7 billion in large-scale renewable and transmission-related projects during the last 10 years.

The Australian Government’s October 2022-23 budget included $20 billion for its ‘Rewire the Nation’ program, a National Reconstruction Fund of $15 billion and the Powering the Regions Fund of $1.9 billion. Likewise, state governments have made numerous significant investments in energy infrastructure including renewable projects, transmission upgrades, storage capabilities and jobs plans.

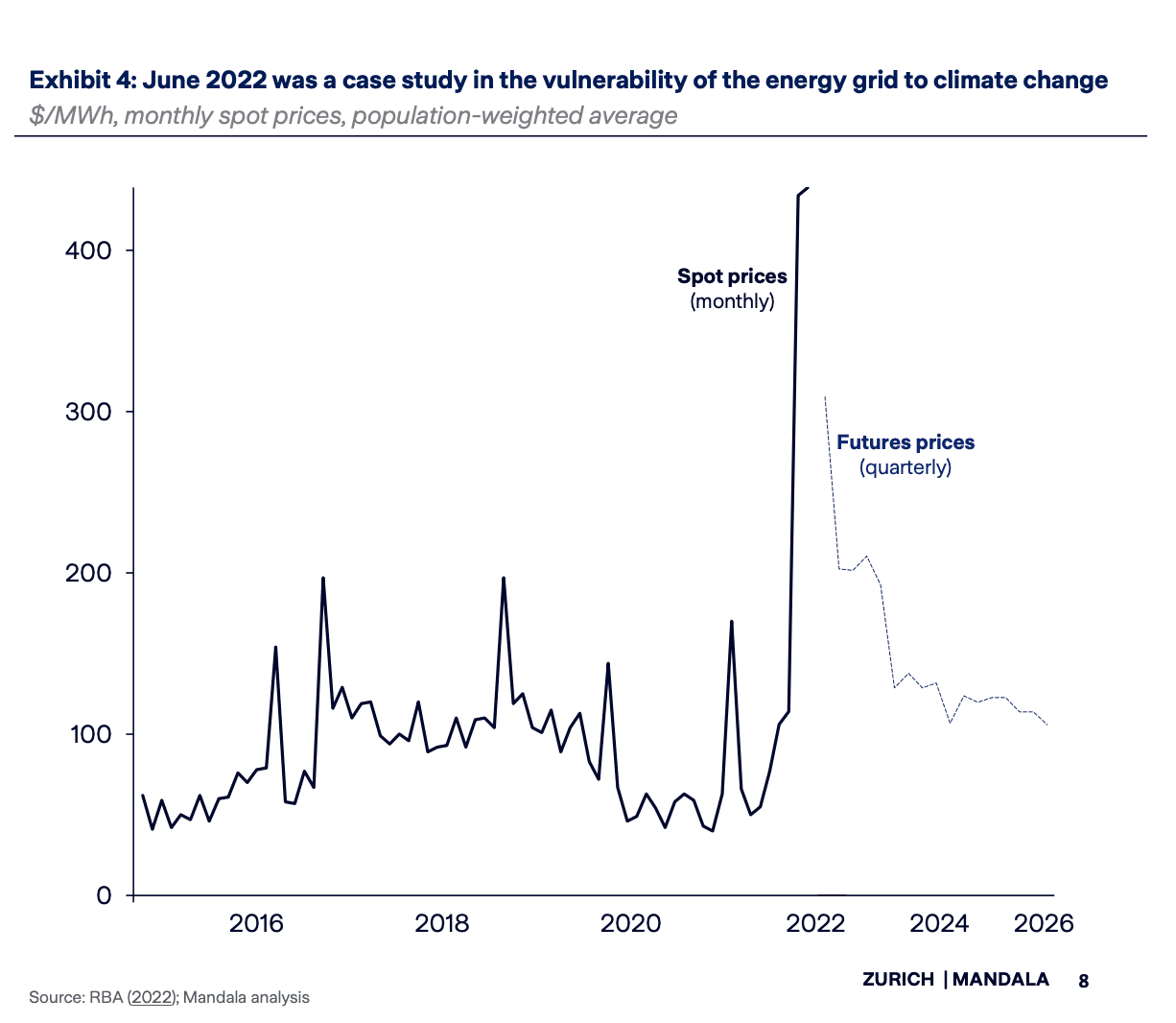

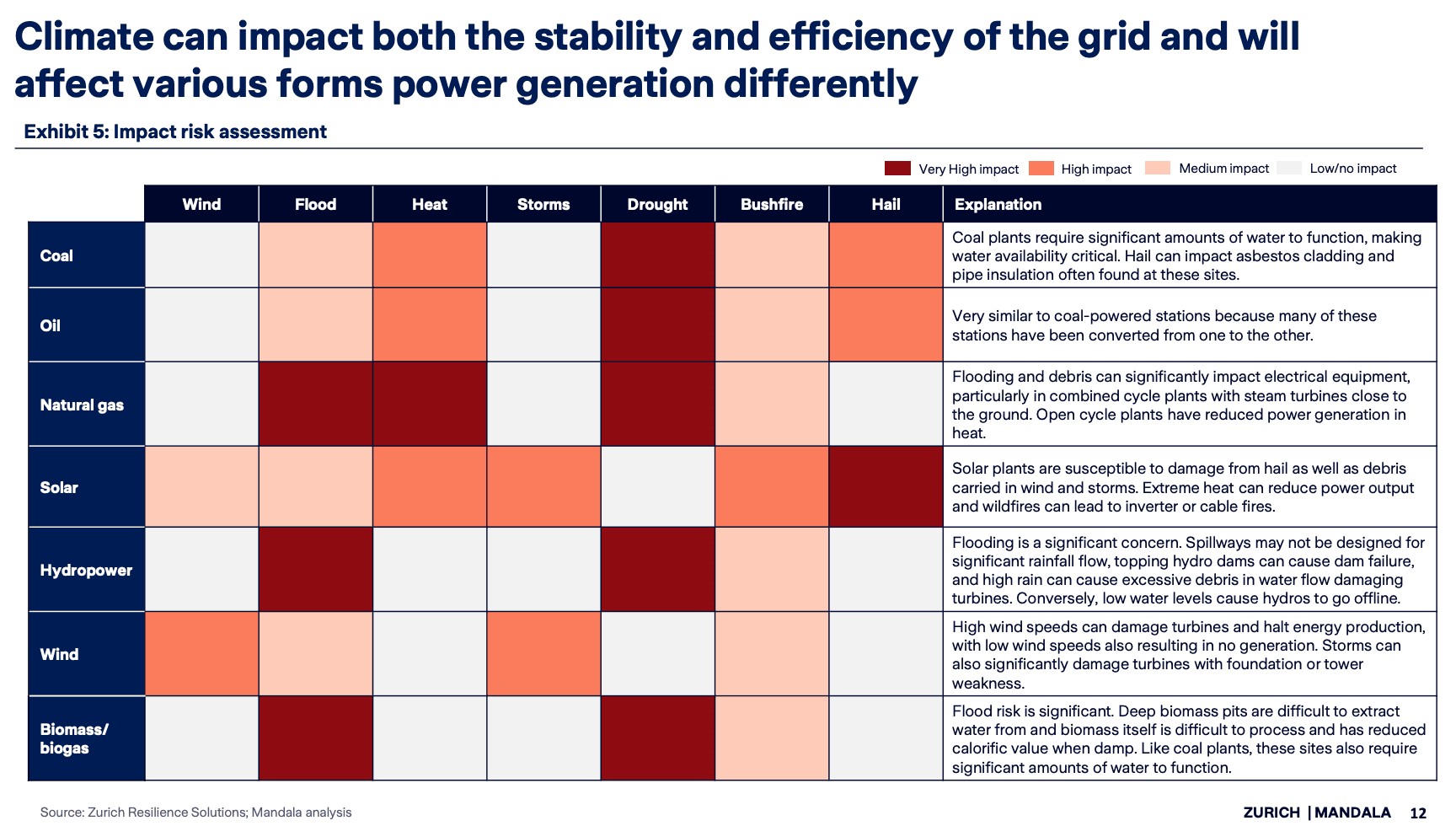

Climate affects the stability and efficiency of the grid, leaving Australia vulnerable to growing climate risk

In June 2022, the monthly average spot price for electricity hit above $350/MWh. In response, the Australian Energy Market Operator (AEMO) suspended the entire National Electricity Market (NEM), declaring the spot market had become “impossible to operate”.

June 2022 was a case study in the vulnerability of the energy grid, showing how a system already disrupted by global factors can be tipped into chaos due to climate-related factors.

Driven by Russia’s invasion of Ukraine, demand and prices for thermal coal sharply increased. Other coal generators faced further disruption due to staff shortages and the impacts of La Niña on coal production. Lower-than expected power generation from renewables also contributed to the overall price increase as adverse weather reduced the efficiency of solar generation. Meanwhile, total demand from the NEM was higher than in previous years. Exceptional rainfall and a series of cold fronts had impacted Queensland and Victoria and led to relatively high total demand from the period.

As these factors drove up prices, the AEMO implemented a price cap for a few days. This led to generators withdrawing from the market and caused the AEMO to suspend the NEM.

Zurich Resilience Solutions (ZRS) provides insights and solutions to help organisations proactively manage and build resilience to traditional and evolving risks, such as climate change and cyber

ZRS global exposure analysis transforms location or asset data into deep climate risk insights. Through a customised and interactive dashboard, businesses and asset owners can understand the probability that climate risks – such as heat, flood and fire – may impact a specific asset or portfolio of locations over different time horizons using three IPCC-based climate scenarios. These insights quantify and contextualise climate exposure to ensure risk can be understood, tracked and shared in order to appropriately prioritise actions and investments.

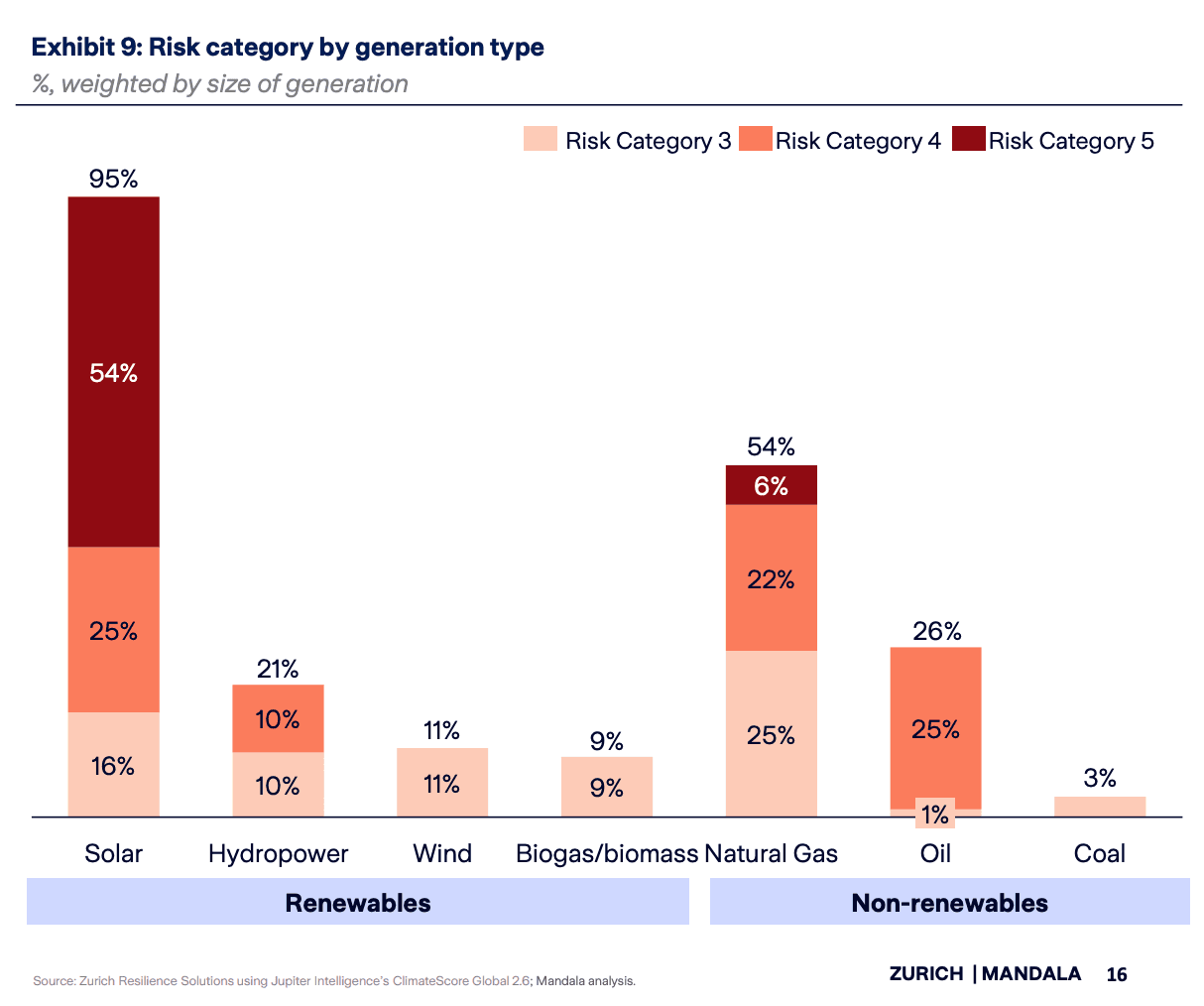

Solar generation is currently most consistently at risk, while coal and biomass are least at risk across Australia

The risk posed by climate perils varies significantly by generation type. Based on the location of current generation sites, solar and natural gas face the highest risk.

The Zurich-Mandala Index found that 95% of solar generation sites were in the three highest risk categories, with 54% in the highest category. This reflects the relative vulnerability of solar panels to numerous perils. Note that this analysis does not include rooftop solar as no granular data is available on its locations. This means that overall risk for solar generation may be more diversified.

The second most at-risk generation types were natural gas and oil, which were found to have 54% and 26% of their generation respectively in risk category 3 and above. This result has been driven by the susceptibility of these generation types to perils such as high temperatures and drought.

Other forms of renewable energy like wind and biogas/biomass sat alongside coal with relatively low risk. A minimal number of these sites were in the highest three categories and less than 1% of generation were in risk categories 4 and 5.

More work must be done to ensure the grid is adapted to the reality of climate change

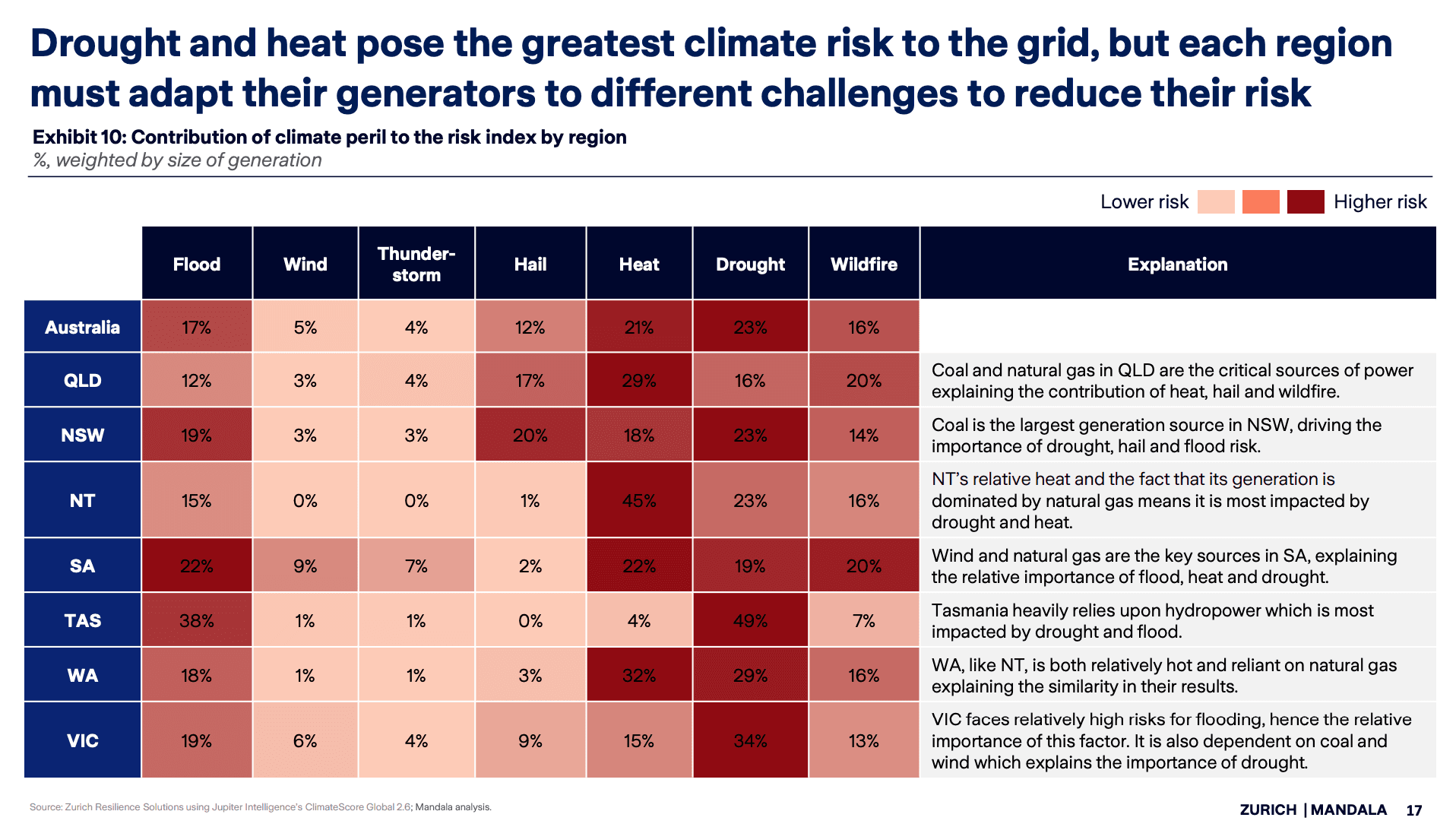

The impacts of extreme weather events caused by climate change put the stability and efficiency of Australia’s energy industry at risk. Extreme weather can impact all points of the energy production and consumption process – including fuel extraction, processing, transportation, generation, transmission and storage, and customer demand. As shown by this report, site selection and planning is critical to ensure new infrastructure is resilient given variability in peril type and severity is significantly impacted by geography. Beyond this, structural and management adaptation measures are also important for building resilience, particularly for existing sites.

This analysis, conducted in conjunction with Mandala Partners, hopefully represents a useful input into achieving an appropriate and resilient energy transition.

Read our latest posts

Time to make a difference: Economic and fiscal benefits of Preventive Care+

Mandala's latest research, prepared for the Australian Self-Care Alliance, examines the economic and fiscal case for Preventive Care+, a proposed health assessment and coaching program for Australians aged 55 to 59. The research finds that early detection and self-care could deliver $233 million in combined health, income and fiscal benefits per cohort over ten years, including $26 million in net health system savings from delaying the progression of four common chronic conditions. Participants could also remain in the workforce for one to three additional years, generating $159 million in additional income, $19 million in additional superannuation contributions and $29 million in additional tax receipts per cohort over ten years. There are funded health checks for 45 to 49-year olds and 75 year-olds, but not for people in their late 50s, a period when chronic conditions frequently emerge and worsen. This report sets out the potential benefits of instituting a health assessment and a coaching program to intervene at a time that can yield meaningful outcomes.

23 Jul, 2026

Unlocking a Virtuous Cycle: Overcoming Barriers to AI in Australian Energy Systems

Mandala's latest research, developed in partnership with Microsoft, examines the barriers to transformative AI adoption in Australia's electricity system. The research finds that AI is one of the few tools able to unlock capacity and efficiency from the existing grid without waiting on new transmission and generation capacity, yet adoption today remains incremental. Three soft barriers, a lack of shared strategy, weak investment incentives and siloed data, are constraining Australia's ability to capture this potential. Overcoming them will require joint action from government, the technology industry and energy utilities to prove AI's value, align policy settings and fund pilots through to deployment.

8 Jul, 2026

Demonstrating the local benefits of AI infrastructure in Wisconsin

Mandala's latest research, prepared for Microsoft, examines the economic impact of hyperscale data center investment on Wisconsin's communities, businesses, and workforce. The research finds that committed data center projects will channel $16.5 billion to local suppliers, support more than 9,000 jobs during construction, and generate lasting economic activity across every county in the state, thereby extending Wisconsin's long tradition of industrial leadership into the AI era.

1 Jul, 2026

The essential infrastructure: How Australian banks power the economy

Mandala's latest research, prepared for the Australian Banking Association, examines the often-hidden role Australian banks play in supporting households, businesses and the broader economy. The research finds that banks are deeply embedded in the financial lives of Australians - as lenders, as community investors, through the jobs they generate and increasingly as assets owned by Australians themselves through shares and superannuation. From financing homes and small businesses to supporting regional communities through hardship and disaster, the report builds a picture of a sector whose success is broadly shared across the Australian population.

17 Jun, 2026